Review

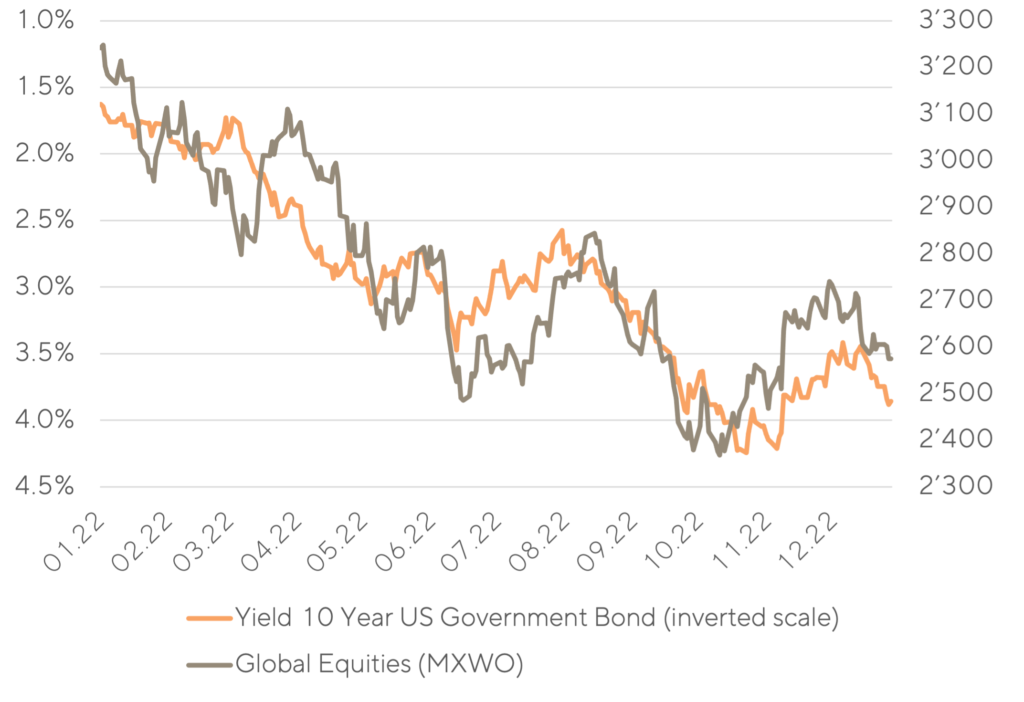

A balanced investment profile aims to offset various influencing factors and stabilize the return. An investor in bonds provides debt capital to companies and is usually compensated with a fixed interest rate. An investor in equities is a co-owner and thus participates in the profits or losses of a company. If the economy grows, corporate profits tend to rise and equities yield a higher return than fixed-interest bonds. In uncertain times, on the other hand, investors seek the safe returns of bonds. Typically, bonds gain in value when stocks perform badly.

Not so this year. Balanced investment portfolios had one of the worst years on record. The reason for this was that the market’s perception changed within a very short period from persistently too low inflation to fear of lasting high inflation. In this context, the very low interest rates of the recent past lost their justification, which caused a strong correction of fixed-interest bonds. Consequently, equities also faltered, because their valuation or earnings yields, are in direct competition with bond yields.

Development of global equities vs. bond yields

The trend of falling interest rates lasted 40 years, peaked with negative nominal yields in some currencies last year and now experienced a dramatic reversal. Accordingly, previous beneficiaries of this trend suffered the most, especially long-dated bonds, expensively valued defensive quality and growth stocks.

Outlook

Now that the U.S. Federal Reserve has raised interest rates at an unprecedented pace, and other central banks around the world have followed suit, the question is how well this interest rate level can be absorbed by consumers, companies and governments. On the one hand, higher interest rates and the increased prices of many goods are straining the budget. On the other hand, the labor market continues to be very robust, wage negotiations are promising, and demand is stagnating at a high level. With China now also easing covid measures, the full impact on demand is difficult to assess at present.

In case the economy weakens, interest rates should stabilize, which would have a supportive effect on equity valuations. However, the development of corporate profits is then likely to be less positive. The various interdependencies between growth, inflation, interest rates and valuations make the current situation challenging. In contrast to the starting position one year ago, bond yields are once again contributing to portfolio returns. The valuation of the stock market reflects the higher interest rate level and, at least partially, the economic slowdown expected by most economists next year.

Conclusion

It is advisable to be prepared for various scenarios and to take a long-term perspective. Current interest rates offer a stable source of income, which is why we have increased the bond allocation and extended our maturities slightly. Due to the sharp rise in interest rates and the resulting changes and risks for the market and the economy, we consider a neutral equity weight to be appropriate at present. Nevertheless, valuations are less demanding and offer good entry points for long-term investors. We expect uncertainties to persist and market developments to remain challenging. However, times like these always offer good opportunities to identify new investments that are at a valuation discount due to the current environment. The resilience of our portfolios remains the upmost priority.

Zurich, end of December 2022